In lending, the deal goes to whoever answers first and follows up cleanest. A merchant fills out an application, you call once, it hits voicemail — and by the time you try again, three other funders already texted them back. Text closes that gap. This guide is narrow on purpose: how lenders, MCA brokers, and loan officers use SMS marketing with the people who want to hear from them — applicants who opted in, your existing borrowers, and your own pipeline.

This is PitchPrfct's blog, so we build SMS software. But the playbook below works on any platform. Lending texting performs best when it's built on opt-in, so that's what the playbook focuses on.

A quick word on the rules

Lending texting works best — and stays healthy — when it goes to people who opted in to hear from you, not to purchased "we fund businesses" lead lists. There are rules around texting cell numbers, and finance is a category carriers watch closely, so it pays to get the basics right. Rather than declare what's legal, we'll point you to the people who set the rules: the FCC's texting rules, the CTIA Messaging Principles, and our TCPA guide and 10DLC guide. This isn't legal advice — check the current rules for your situation. With that settled, the rest of this guide is about the texting that actually converts: people who raised their hand.

Where the best lending lists come from

The list that performs is built from people who opted in to hear from you:

- Applicants who consented at submission. Your application form, funnel, or intake page with a clear, separate SMS opt-in checkbox — documented with a timestamp and source.

- Current and past borrowers. The book you've already funded is your best, safest list: renewals, re-ups, additional positions, referrals.

- Your own pipeline and clients. Brokers who've worked a relationship — not a list someone sold you last week.

Keep records of consent (timestamp + source) and scrub your list before every send — both are good practice. Segment from day one: a fresh applicant mid-underwriting, a funded merchant 60% through their term, and a client who paid off last year are three completely different conversations.

The four moments where texting earns its keep

1. Speed-to-lead on new applications

This is where lending texting pays for itself. A lead contacted within five minutes is 21× more likely to qualify than one contacted at 30 minutes (Harvard Business Review). An automated text fires the instant an application lands — so even at 9 p.m. on a Friday, the applicant hears from you before the next funder does, and a human picks it up from there.

2. Document and stip collection

Deals die in the stip stage. Bank statements, the signed application, a voided check — chasing those by email is where momentum goes to stall. A short, specific text ("we need your last 3 months of bank statements to move forward") gets a reply in minutes, not days, and the whole back-and-forth lands in one thread.

3. Approval and status updates

Silence kills trust in funding. A quick "you're approved, here's the next step" or "your file's in underwriting, I'll update you by EOD" keeps the merchant warm and stops them from shopping the offer elsewhere while they wait.

4. Renewals and re-ups

Your funded book is recurring revenue if you work it. A heads-up as a merchant approaches the renewal window — when they're paid down and eligible for more — is the highest-margin, easiest text you'll send, because it's going to someone you already have a relationship and consent with.

Texts that actually get replies

Compliance gets the message delivered; craft gets the reply. What works in lending:

- Identify yourself every time — name and company. ("Hi {{name}}, it's Marcus at Keystone Capital.")

- One idea, one ask, under 160 characters.

- Be specific — name the exact stip, the exact next step, the exact amount.

- Skip the hype — no guaranteed-funding language, no false urgency. It gets campaigns blocked and erodes trust.

- Personalize with merge fields — name, business, the document you need.

Lending scripts you can adapt

These assume the contact opted in and end with an easy opt-out:

- New-application speed-to-lead: "Hi {{name}}, it's {{rep}} at {{company}} — got your application for {{business}}. I can walk you through options now. Good time to talk? Reply STOP to opt out."

- Document / stip request: "Hi {{name}}, to keep your file moving we just need your last 3 months of business bank statements. You can text them right here. Reply STOP to opt out."

- Approval / status update: "Good news {{name}} — your file's approved. I'll send terms in a few minutes; reply here with any questions. Reply STOP to opt out."

- Renewal / re-up: "Hi {{name}}, you're paid down enough on {{business}} to qualify for more capital. Want me to pull together a renewal option? Reply STOP to opt out."

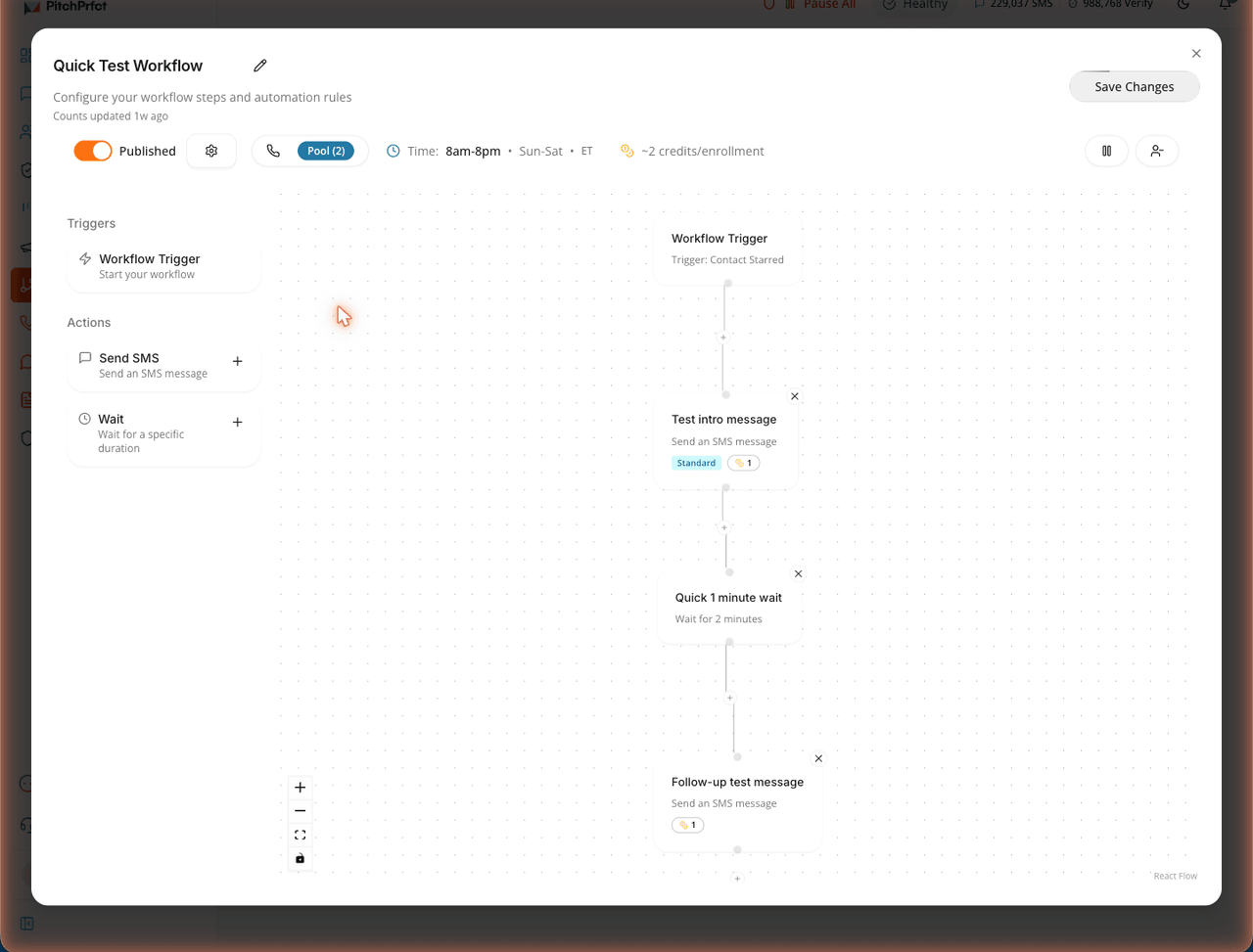

Put it on autopilot — without losing the human touch

The lenders who scale texting use automation for timing and humans for the conversation. A good platform lets you trigger an instant text the moment an application lands, nudge for stips on a delay if a document hasn't come in, fire status updates off pipeline stages, and queue renewal outreach against the term date — all with merge fields filled in and opt-outs handled automatically.

That mix is where SMS marketing stops being a chore and starts compounding. Build a small library of SMS templates for the moments that repeat — new application, stip request, approval, renewal — and wire your loan CRM or LOS in so the texts fire off real events.

See the whole thing end to end:

Where PitchPrfct fits

PitchPrfct is a compliance-first SMS platform built for any business that sells — lenders and brokers included:

- Setup handled for you: automatic opt-out (STOP) handling, quiet-hours enforcement, and list scrubbing, plus guided 10DLC registration — the best-practice setup that matters most in a category like finance.

- Workflows + a conversations inbox for speed-to-lead, stip collection, status updates, and renewals — automated timing, human replies.

- Connects to your loan CRM/LOS: Zapier, Make.com, a REST API, and webhooks wire your texting into the systems you already run on. And Jayni, our AI assistant, is live. (It's SMS-only — no email channel.)

- Flat, predictable pricing: $99/mo + $0.007 per segment, all-in (carrier fees included). Like any platform, $1/mo per number and the standard $10/mo TCR campaign fee apply on top; unused credits roll over one month. See the full pricing breakdown.

It's SMS-first by design — not a full lending CRM or dialer — so if your day runs on cold calling, pair it accordingly. For texting your opted-in applicants and your funded book, it's purpose-built. If you came from the insurance side of financial services, the same playbook carries over — see our SMS marketing for insurance agents guide.

Frequently asked questions

How do I set up SMS marketing for lending the right way?

Should I text a purchased list of business-loan leads?

Do the rules apply to B2B lending texts?

How fast should I text a new loan application?

What should a lending text say?

Want opt-in speed-to-lead texting with the setup handled for you? Start a free trial.